The VA home loan is a type of mortgage loan offered exclusively to military personnel in return for their service to the country. Because the loans are backed by the U.S. government, lenders can offer more favorable terms but still be protected should a borrower default on their loan. Of course, defaults sometimes happen, and that’s where the VA Funding Fee comes in.

The VA Funding Fee is a one-time, non-negotiable fee applied to each VA Purchase Loan, Cash-Out Refinance Loan and Interest Rate Reduction Refinance Loan (IRRRL); it is paid directly to the Department of Veterans Affairs to help cover defaults. This eases some of the burden on taxpayers and enables the VA Home Loan Guaranty program to remain available to current and future military home buyers.

Is the VA Funding Fee always the same?

No. The fee will vary based on a handful of factors: the type of military service, the type of loan for which the borrower is applying, if there is a down payment (which may decrease the fee), and whether the borrower is a first-time user or has used the VA home loan benefit previously. It is also important to note that Reservists and National Guard members will pay slightly more than regular military members.

Here is a breakdown of the VA Funding Fee for Purchase and Construction Loans:

| Type of Veteran | Down payment | Percentage for First time use | Percentage for Subsequent use |

| Regular Military | None 5% or more 10% or more | 2.15% 1.50% 1.25% | 3.3%* 1.50% 1.25% |

| Reserves/National Guard | None 5% or more 10% or more | 2.4% 1.75% 1.5% | 3.3%* 1.75% 1.5% |

For Cash-Out Refinance Loans and IRRRLs, you can view the VA Funding Fee Table here.

Do all military buyers have to pay the fee?

No. Veterans receiving VA compensation for a service-connected disability are exempt from having to pay the VA Funding Fee, as are those who would be entitled to receive such compensation if they were not collecting retirement or active-duty pay. Surviving spouses are also exempt if their husband or wife died in service or from a service-connected disability.

Your lender will be able to verify your VA Funding Fee status during the loan process, typically by looking at your Certificate of Eligibility (COE).

When is the VA Funding Fee due?

The fee is due at closing and collected by your lender, who then automatically transfers the payment directly to the VA. In cases where an exemption status is awaiting approval—for example, because of a pending disability claim—the borrower must still pay the fee at the time of the closing and will be issued a refund if the claim is later approved.

How can I pay it?

Borrowers have a few options for paying the VA Funding Fee. They can pay the fee out of pocket, ask the seller to cover the fee on their behalf, or finance the fee and roll the cost into their total loan amount. (The VA Funding Fee is the only closing cost that can be rolled into the home loan.) Most VA borrowers choose to finance the fee, even though their monthly payments will be slightly higher as a result.

Remember, your VA Funding Fee status is determined by your COE.

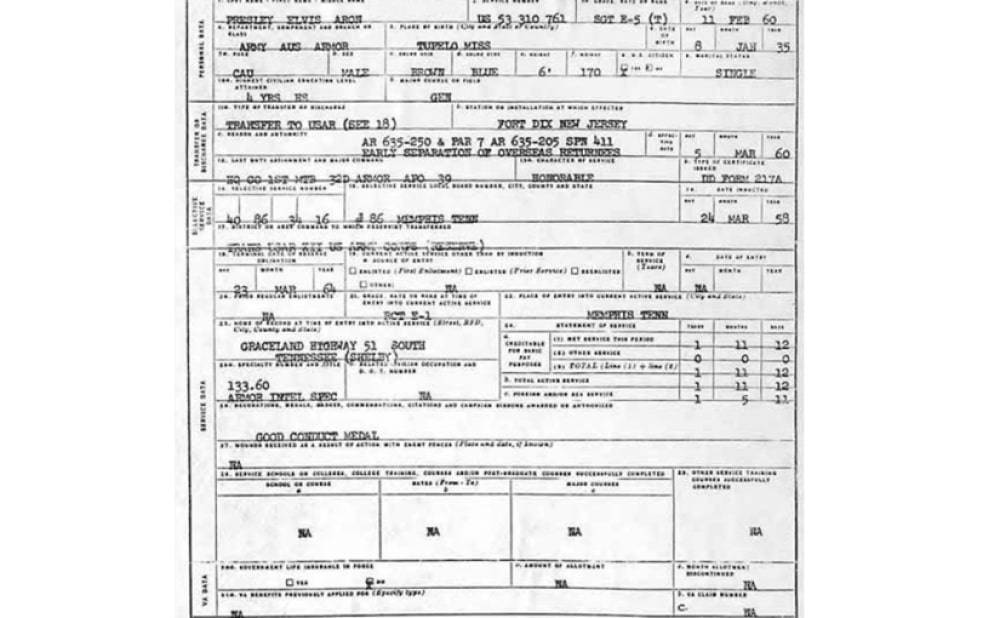

In order to obtain your COE, you will need to provide specific documents that prove to the lender you are eligible for VA mortgage assistance. Specifically, veterans will need a copy of their DD214 showing both the character of service and the narrative reason for separation.

Veteran-owned DD214Direct helps you get the documents you need, when you need them.

Our cutting-edge technology platform and keen knowledge of government protocol and procedure allow us to deliver your documents faster than competitors. We physically stand in line at the records repository and manually coordinate your order, freeing up your time and easing your worries about whether or not you will get your DD214. Much like paying a small fee to have your taxes done by a professional, DD214Direct provides the service and convenience you’ve been hoping for, plus we make it a lot easier.

Instead of having to download, print, sign and fax your document request form, you can submit your order directly through our website with the ease of e-signature technology from a desktop, laptop or mobile device. Once we locate your DD214, we will email you a copy immediately—a service not offered by the government. And tracking your request through us is simple, so you never have to worry about long hold times and inconclusive answers.

Ready to get started? Click here to begin the order process.